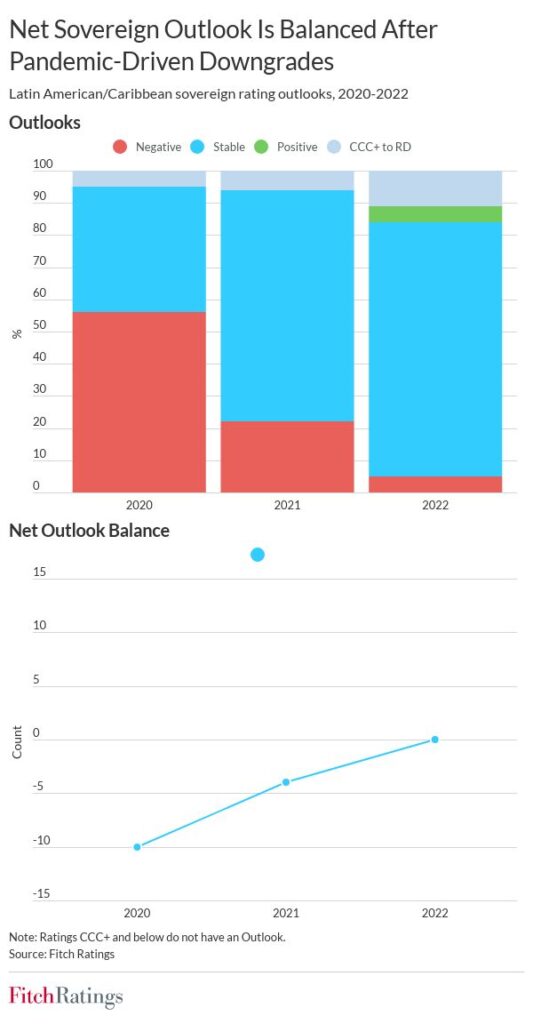

January 10, 2023

Proactive monetary tightening, expected lower inflation, steady external buffers and flexible exchange rates, and 2022’s stronger-than-expected fiscal performance will help Latin American sovereigns navigate increasingly challenging global conditions next year, Fitch Ratings says. This is reflected in Fitch’s neutral 2023 sector outlook, although political uncertainties, wide current account deficits, and the erosion of external buffers are a vulnerability for some sovereigns. The balance between Positive and Negative Rating Outlooks is even, at one each.

We expect there to be a considerable economic slowdown in 2023. A mild US recession will be negative for Mexico and other Central American and Caribbean countries where trade, financial, and remittances linkages remain strong, while subdued Chinese growth will weigh on South America. More positively, external and domestic factors, including aggressive policy tightening by several central banks, should reduce inflation in most Latin American countries.

Fiscal consolidation will slow amid weaker growth, lower commodity prices, continued spending pressures and rising borrowing costs. Fitch projects a median 2023 fiscal deficit of about 3% of GDP, in line with the average of the regional median during 2015-2019, but most sovereigns’ debt burdens will broadly stabilize, having jumped during the Covid-19 pandemic. Brazil’s fiscal and debt trajectory under the incoming Lula government remains uncertain.

Low-rated sovereigns, many of which have lost market access (Argentina, Ecuador and El Salvador) or those with large current account deficits, are more vulnerable to tightening external conditions. Elsewhere, high real interest rates, flexible exchange rates, sound external buffers, and access to multilateral borrowing should underpin shock-absorption capacity.

Governability challenges, political gridlock and instability, and social mobilizations remain risks. The ascent of left-leaning governments increases the scope for microeconomic interventionism, as seen in Mexico, and policy uncertainties remain in Chile and Colombia. Argentina’s capacity for significant policy adjustments will remain uncertain after the 2023 election.