January 10, 2023

The 2023 sector outlook for Latin American (LatAm) banks is neutral, as core credit drivers in most countries across the region are expected to remain relatively stable despite continued deceleration in economic growth and lingering inflation, Fitch Ratings says.

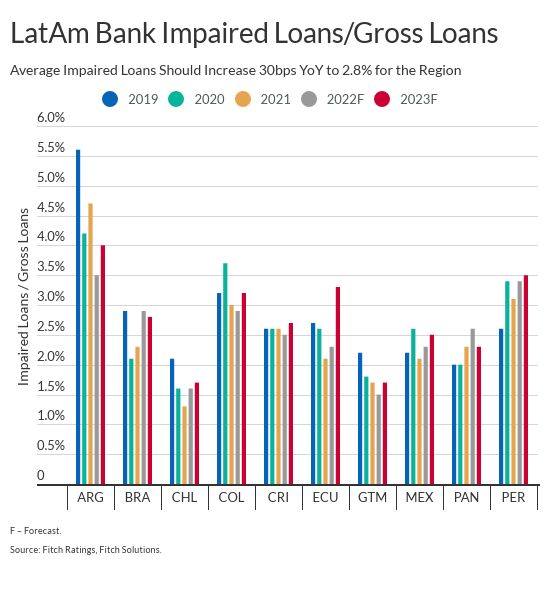

The region’s banking sector key financial metrics should remain relatively stable as normalizing credit costs will be absorbed by loss provisions that were built during the pandemic and continued healthy levels of profitability. However, the expectation of sustained balance sheet growth, higher dividend payments and a likely increase in loan impairments due to unseasoned retail credit growth since 2021 could weigh on bank capitalization levels in 2023.

Fitch expects median LatAm GDP growth to decelerate to 2.4% in 2023, after declining to 3.7% in 2022 from a 9.2% rebound in 2021. Additionally, Fitch anticipates a decline in the region’s average median inflation rate to the mid-single digits in 2023, from high single digits this year. Nevertheless, growth risks are skewed toward the downside given the anticipated U.S. recession in 2023.

Argentina, Colombia, Ecuador and Peru have deteriorating sector outlooks, reflecting weaker economic prospects amid political and policy uncertainty, which could increasingly pressure bank performance in these markets. Conversely, none of the markets covered in this report have an improving sector outlook.

Key items to watch include potential effect of longer-than-anticipated higher inflation and interest rates, increasing recession risks that further stress borrower repayment capacity, seasoning of accelerated retail loan growth in less favorable operating environments and progress in implementing Basel III capital standards regionwide.

Fitch assigns investment grade Long-Term Issuer Default Ratings to only about 29% of internationally rated LatAm banks. Of these, 18% are driven by sovereign support, 33% are driven by institutional support and 49% are driven by the banks’ standalone creditworthiness.