By Kimberly Ramkhalawan

The recent uptick in mergers and acquisitions happening in Trinidad and Tobago has prompted its Central Bank to introduce some guidelines aimed at regulating these types of transactions. In what seems to be a wave of mergers and acquisitions happening around the globe, the Trinidad and Tobago Central Bank sought to discuss its role as regulators of these transactions and the implications it can have on markets.

With the first quarter of 2021 already seeing two major acquisitions occur where the sale of assets of the Eastern Caribbean subsidiaries of the Canadian-owned, T&T based RBC Financial Caribbean Limited to a consortium of indigenous banks in the Eastern Caribbean, as well as local ANSA Merchant Bank’s acquisition of Indian owned Bank of Baroda, questions have been asked on what has been happening within the TT finance landscape.

The sale of the Indian bank seemed to be a lucrative one, as it entailed some of its overseas subsidiaries as part of the package to rationalize the bank’s operations.

A similar trend was followed when Republic Bank Limited acquired a majority in Cayman National Corporation, as through this move it is now able to access markets in the Isle of Man and Dubai. The group Republic Financial Holdings (RFHL) also acquired Scotia’s operations in several Eastern Caribbean states, including Anguilla and St. Marteen. In 2020, the RFHL would also gain hold of Scotia’s operations in the British Virgin Islands as part of its drive to expand its operations in the wider Caribbean, and gain international presence.

Apart from banks, Insurance companies also saw their fair share of takeovers, as Guardian Holdings Limited was acquired by Jamaican owned NCB, Sagicor taken over by Canadian based Alignvest, MotorOne obtained by Jamaica’s General Accident Insurance Company along with Trinidad and Tobago based MICON Marketing Limited, and Beacon Insurance Limited acquired by Bermuda’s Colonial Group International Limited, now known as Coralisle Group.

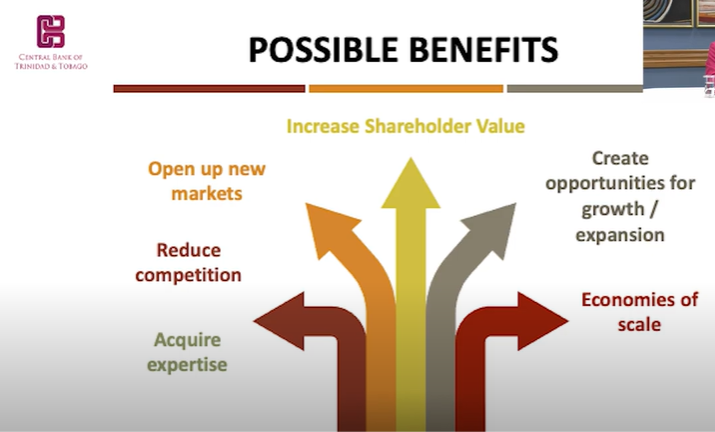

According to Michelle Francis-Pantor, who serves as Deputy Inspector of Banks, Non-Banks and Payment Systems Oversight at the Central Bank, these latest moves indicate that while local financial institutions are looking to broaden their presence regionally and internationally, Trinidad and Tobago has also been attracting Foreign companies who see it as a lucrative market.

But she says not all acquisitions have been successful, as Republic Financial Holdings attempts to acquire Scotia’s operations in Guyana was terminated by the Bank of Guyana, as concerns over systemic risks surrounding market concentrations were raised, stating that had the transaction taken place, RFHL would have had over 50 percent ownership of the assets and deposits of the Guyanese Financial sector.

Meanwhile, the proposed takeover of ScotiaLife by Sagicor was terminated by mutual agreement and the proposed sale of a majority stake in FCIB by CIBC by Columbian owned GNB Financial group, did not obtain regional regulatory approval. She adds that generally regulators do not disclose the reasons for the objections to a merger or acquisition publicly, but may opt to do so where public interest and stake such as potential for systemic risks or potential impact on competition.

Francis-Pantor says red flags are often raised over the possibility of an organization gaining over 50 percent of the market share, as it creates a situation where it has too much footing for the bank in the market and a possibility for monopolization, which leads to other concerns arising as a result of this, such as job redundancies, the welfare of employees, customers and other stakeholders.

Such systemic risk issues factor into any decision it makes whether to approve the transaction or not. At this point, once market share is greater than or equal to 40 percent, the Central Bank says any moving forward requires consultation with the TT Minister of Finance for approval, as the Ministry has the final say taking into consideration the state of Financial services and the interest of consumers within the local market.

But what happens when an institution organically grows beyond the 40 percent threshold, just how are the risks mitigated? Francis-Pantor she says an assessment

is done on its impact on the system, and the TT Central Bank as regulators would consider whether the institution has the capacity for the overall impact on the financial system.

Apart from that, the size and concentration of economic power for acquisitions will prevent or lessen substantially, competition of financial institutions in Trinidad and Tobago. Customers are left with little choice in financial services offered within the local landscape, while systemic risk also arises, as being ‘too big to fail institutions’ are now created resulting in financial stability concerns.

The expected benefits of the acquisition may not occur within the desired speed and expansion may never materialize, resulting in reputational risk when things do not go to plan along with diminishment of the brand’s strength. Differences in corporate culture that might not be easy to consolidate or integrate can also be another contributing factor.

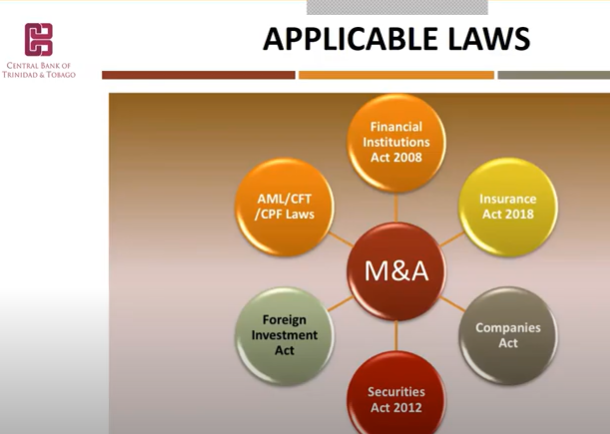

Current legal frameworks include the Financial Institutions Act 2008 and the Insurance Act 2018. In Trinidad and Tobago such moves consider the Anti-Money Laundering Act (AML) which focuses on combating the funding of terrorism (CFT), and proliferation financing laws (CPF).

Highlighting how these work in mergers and acquisitions, Alisha Corbin Connelly, Senior Examiner at the Office of the Inspector of Financial Institutions, says under the Financial Action Task Force (FATF) uidelines, all jurisdictions are required to comply with a certain legal framework that requires due diligence and scrutiny of transactions to ensure that financial institutions are not subject to unscrupulous persons and undesirable practices, while black and grey listed individuals and organizations may have implications for non-compliance with these laws and may rebound at a country level where correspondence banking may be affected by this. However, she adds that the Central Bank pays particular attention in its assessment of companies’ compliance to the AML, CFT, CPF requirements for proposed acquirers and controlling significant shareholders.

She adds that the Securities Act 2012 are triggered when an acquisition amounting to 30 percent of shares in a public company and results in a number of issues for the proposed acquirer, including publication of the order over a period of time and shareholders would have a right to purchase shares. The plus of this, is that is also offers protections of shares held by minority shareholders. Other checks and

balances can be found in the Companies Act, which plays a pivotal role as an overarching piece of legislation that affects any registered company, covering any change of names, shareholder rights, vertical and horizontal amalgamations.

As for foreign companies entering the market, institutions should also ensure the Tax Information Exchange Agreement United States of America Act, and the Income Tax Act and other laws are examined along with FATCA and common reporting standards requirements involving financial institutions while making certain disclosures to the Board of Inland Revenue for remissions to overseas jurisdictions including the United States. Corbin- Connelly adds that the Corporate Tax Act may affect some transactions and financial institutions will need to be cognizant of cross border issues related to taxes. For this, she says the Foreign Investment Act is also important where an investor is seeking to acquire 30 percent or more in shares in a local company, something they must obtain a license from the Ministry of Finance, while certain exemptions do apply to certain CARICOM states.

As for Insurance Companies, once a merger or acquisition involves a licensee or insurer approval is required, the Central Bank is required to assess any proposed change in ownership of a controlling or significant shareholder of any licensee, insurer or financial holding company.

The Fair-Trade Commission is another regulator which works alongside the Central Bank and any bank licensed under the Securities Act falls outside the scope of the FTA. However, this does not apply to insurance companies which is not mentioned in the FTA with respect to mergers. The FTA applies to all mergers and registrants and looks at anti-competitive agreements and monopoly practices.

Exploring the deciding factors needed to approve an application, Kendall Cuffy, Manager of Banks and Non-Banks says supervisory guideline’s pinpoint to corporate governance, liquidity risk, fitness and propriety and market conduct.

As regulators, Cuffy says while they look for financial soundness through asset quality, liquidity and earnings and profitability, it is Capital Adequacy that indicates the level of protection against risk such as risk to depositors, policy holders, creditors and other stakeholders. Ensuring adequate levels of capital both on a solo and consolidated basis promotes financial stability and it maintains public confidence in the licensees and insurance companies.

He adds that the capacity of the applicant can be told by a few key things, including how is the acquisition being funded, is borrowing involved or are they using their own funds, will the transaction result in it being overleveraged?

The applicant’s ability to provide current and ongoing support for capital adequacy and other financial requirements both pre and post restructured is of critical importance. Other key factors reviewed are the dividend policy of the acquirer and the proposed dividend policy for the entity being acquired or merged, along with a projected balance sheet, earnings and cashflow statement. The Central Bank says it will also need to understand any economic and statistical model used to evaluate risk.

Transparency of ownership is a requirement, citing the Panama papers as reason for knowing who the investors are and their backgrounds whether there might be possibility of fraudulent and offshore accounts to mask their activity, at the end identification of the ultimate owner must be listed. Directors must have competencies when it comes to managing such an institution, such as qualifications and experience in understanding market and product knowledge, while any charges and convictions are viewed not desirable for applicants.

He however cites the company’s IT plans as pivotal for any business transfer, as it poses the greatest risk for any business, and can often result in a negative impact on all stakeholders if it does not go well. IT systems are required to provide information that is accurate, timely and relevant to manage institutions risk, and a seamless integrating system and the degree of how much manual intervention is required is also examined.

Cuffy sought to explain why they are very particular when it comes to market shares. He says any systemic and concentration risk can increase share prices of the acquiring company in the short term, however, these events could further reduce market debt, constrain liquidity and increase market and risk concentration. This he says can reduce stability and result in a domino effect in that group if there is an issue with the controller or one of the partnering entities in the group, which can also lead to monopolistic behaviour, making the determining factor in market shares not limited to income, assets, funds, total policy liability.

As for institutions that are part of a mixed conglomerate group where it engages in both financial and non-financial entities, in such an instance, the bank says the financial operating companies of the group must be fenced from the non-financial entities, by establishment of a financial holding company.

Where parallel owned banking structures exist, banking and insurance companies are licensed in different jurisdictions but have the same beneficial owners and share common management in interlinked businesses, but are not part of the same financial group for regulatory consolidation purpose, the Central Bank will look at intergroup exposures and whether they result in capital income or assets being inappropriately transferred from the regulated entities in the group to unregulated entities, or whether there is evidence of overleveraging of capital.

Given these overlapping issues present, the Central Bank says it will collaborate with regional regulators for the approval.

The latest exit by big names such as Royal Bank of Canada, and its selling of its banks to regional brands that may not be so strong and sends a different kind of message to the public. Concerns raised over the kind of parties that will now look at the region for investment, Francis-Pantor says while the Central bank remains open to different players looking to enter the market, emphasis will be placed on the institution’s fitness and propriety.

But what happens if a company performs poorly post a merger? Cuffy says the Central Bank will manage it according to its regulatory framework, while they will assess the liquidity and quality of assets. As for the company doing the acquiring of the poor performing entity, he adds that it will look at how much value it will be adding and the extent the merger will improve the performance of the poorer entity when combined.

And if a merger flops and each entity looks to part ways? Francis-Pantor says this is considered crisis management and in such a situation, consideration would be looked at where the institution could be returned to one of soundness, along with sound credential ratios.

Francis-Pantor made it clear that the Central Bank will not tell an organization whether it has been over or undervalued, as the bank does not engage in evaluating entities up for acquisition and mergers. She adds that the norm is for this to be

documented in the sheer purchase agreement or their amalgamation agreement, telling how the takeover will be funded.

As to one that has been undervalued, this often falls squarely on the shoulders of the shareholders who would have had to agree to the value placed and is described as part of the company’s due diligence. At this point it is understood that the board would have come to its resolution and action which caters to the impact it will have on shareholders, the financial system, policyholders and depositors.

For companies looking at conducting any merger and acquisition, the TT Central Bank says while it understands the level of secrecy needed on the business move, it’s advice to all players close or near the transaction, the Central Bank asks to be kept abreast of the ‘deal’, and should be approached, informing them that such a business move is currently on the table. Francis-Pantor says seeking guidance from an early stage, will speak to the application and help build the regulatory relationship as well. She adds the bank frowns upon hearing such news in the daily print.

The Central Bank says its operations has remained up to international standard and comparable to its counterparts around the world. However, it hopes that is it has assisted the process by putting forward this information in the public’s domain, which can be accessed via its website, making it a little more efficient for those looking to do business with local institutions.